China’s 3rd Plenum—Three Takeaways for Latin America

China’s 3rd Plenum sets the course for Chinese economic policy over the next five years. What will China’s plans mean for Latin America?

The Dialogue’s Asia & Latin America Program engages and informs academics, policy-makers, and private sector leaders from Latin America, the United States, and across the Asian region on evolving themes in Asia-Latin America relations. Our working group meetings, events, and publications seek to address areas of critical interest and to identify shared priorities on both sides of the Pacific. To receive our latest on Asia & Latin America, please sign up to receive our program newsletter.

China’s 3rd Plenum sets the course for Chinese economic policy over the next five years. What will China’s plans mean for Latin America?

Miguel Otero-Iglesias and Agustin Gonzalez-Agote discuss China’s currency internationalization ambitions in this guest blog post for the Inter-American Dialogue’s Asia and Latin America Program.

How will the new China-Caribbean Development Center affect China’s relations with the region?

A Latin America Advisor Q&A featuring experts’ views on China-Ecuador relations.

Margaret Myers, director of the Asia & Latin America Program, was interviewed by Esteban Lafuente of La Nación on the challenges and opportunities resulting from China’s shifting engagement with the region.

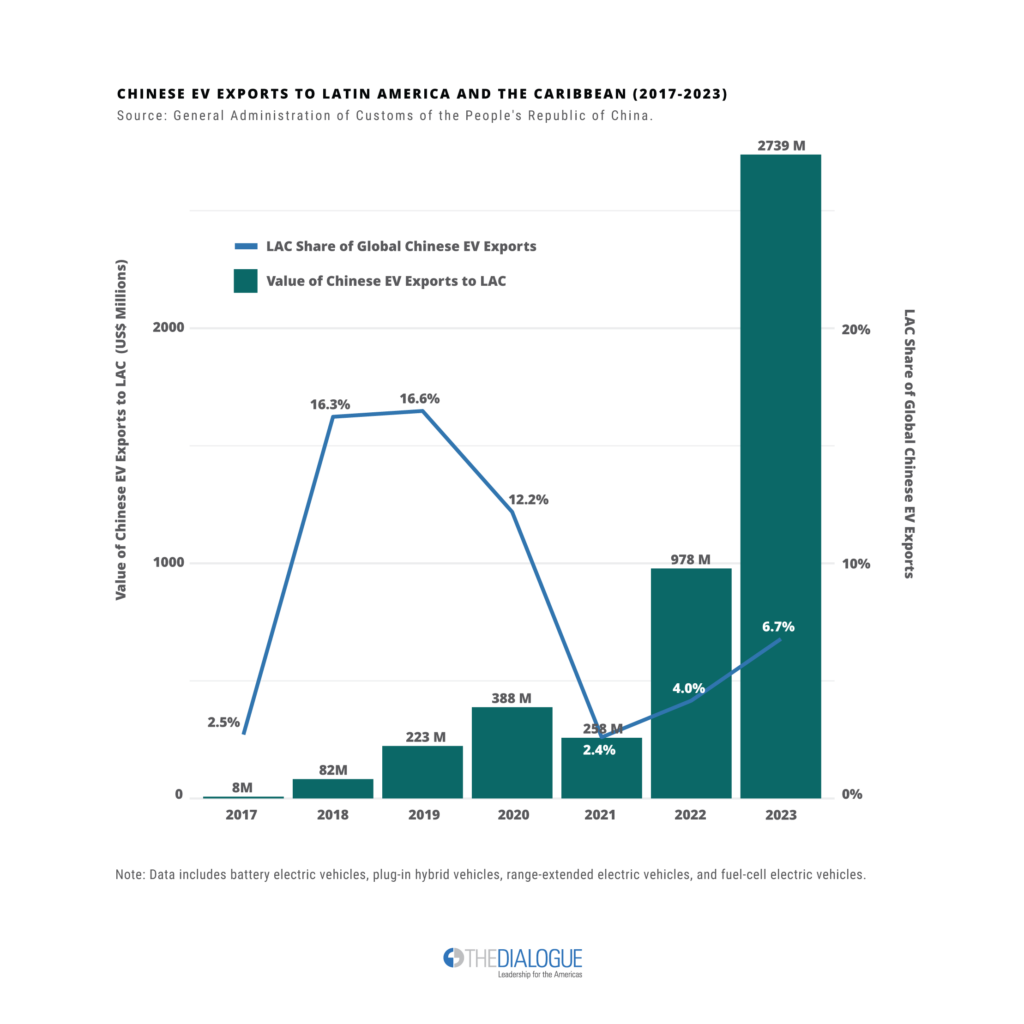

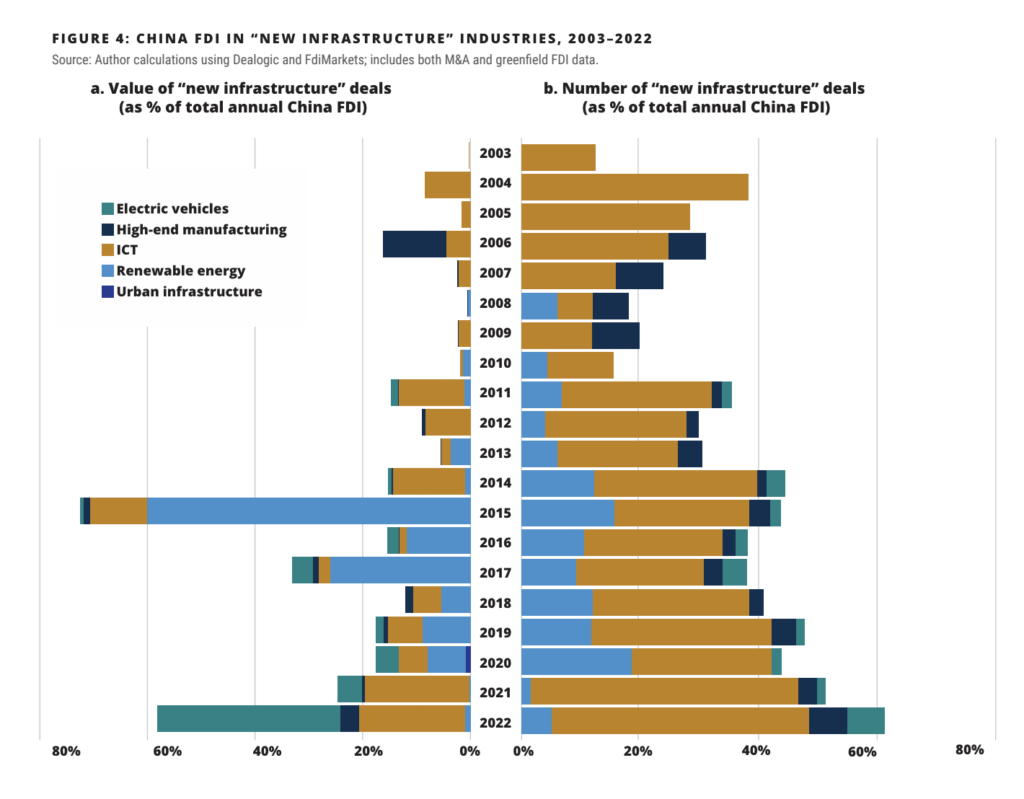

China’s attempted economic recalibration has already reverberated across the Latin American and Caribbean region, as many countries see new interest from Chinese companies in emerging industries. Asia & Latin America Program Director Margaret Myers considers the increasingly uncertain role of Central America in this new equation.